Company Newsair quality monitoringsmart citiesmarket researchBerg Insightenvironmental monitoringurban air quality

Sensorbee Featured in Berg Insight Smart Cities Market Report

Posted by David Löwenbrand on · 6 min read

Sensorbee has been profiled as one of the key vendors in Berg Insight's newly published market report, Smart Cities: Connected Public Spaces – 4th Edition. The 270-page study — featuring five-year forecasts, 123 company profiles, and insights from 50 executive interviews — identifies urban air quality monitoring as the fastest-growing smart city segment, with a compound annual growth rate (CAGR) of 25.2 per cent through to 2029.

For Sensorbee, inclusion in this independent market research report represents third-party validation of our position in a rapidly expanding global market.

Air quality monitoring: the fastest-growing smart city vertical

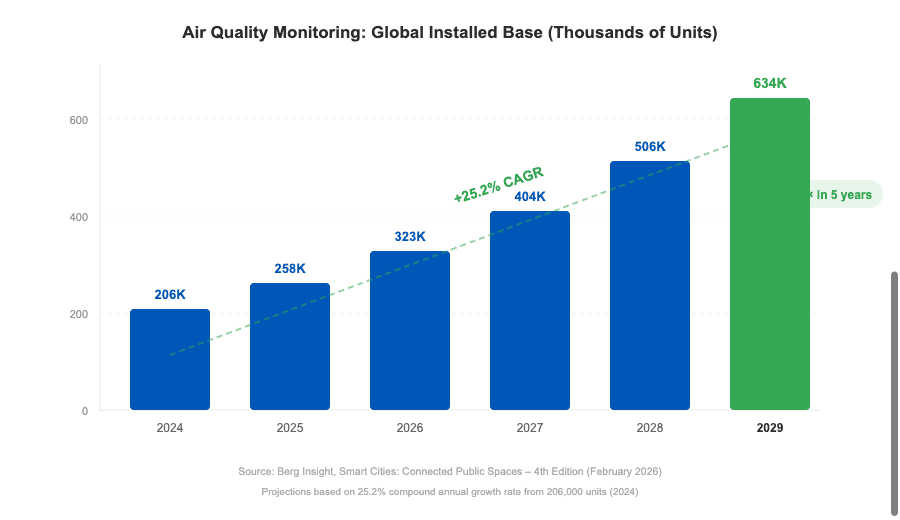

The global installed base of networked, non-regulatory air quality monitoring devices reached 206,000 units in 2024. At the current growth trajectory, that figure is projected to surpass 634,000 units by 2029 — more than tripling in five years.

What is driving this expansion? Traditional air quality monitoring has long relied on expensive reference-grade stations costing upwards of £100,000 each, deployed at only a handful of locations per city. The emergence of affordable, compact, networked monitoring devices has fundamentally changed the equation. Cities can now deploy dense monitoring networks at a fraction of the cost, delivering real-time spatial coverage that was previously impossible.

Europe leads adoption, followed by North America and China. The UK market is particularly active, driven by Clean Air Zones, Low Emission Zones, and tightening Local Air Quality Management (LAQM) requirements under the Environment Act 2021.

How air quality monitoring compares to other smart city segments

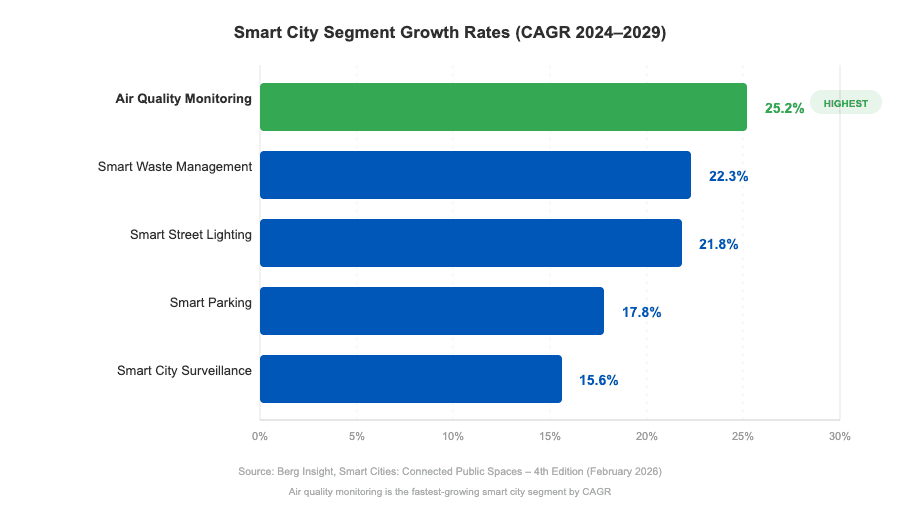

Berg Insight analyses five key smart city verticals in the report. Here is how they compare by growth rate:

Segment

Installed Base (2024)

CAGR

Projected (2029)

Air Quality Monitoring

206,000 units

25.2%

~634,000 units

Smart Waste Management

1.6 million units

22.3%

4.3 million units

Smart Street Lighting

27.9 million units

21.8%

74.5 million units

Smart Parking

1.5 million units

17.8%

3.4 million units

Smart City Surveillance

€13.6 billion

15.6%

€28.0 billion

Air quality monitoring has the highest growth rate of any smart city vertical tracked in the report. Whilst it is currently the smallest segment by installed base, this reflects both the earlier stage of market development and the significant runway for expansion ahead.

What is driving the growth

Several converging factors are accelerating adoption of urban air quality monitoring networks worldwide.

Regulatory pressure

The EU's revised Ambient Air Quality Directive sets stricter limits for PM2.5 and NO2. In the UK, Clean Air Zones in cities like Birmingham, Bristol, and Bath are creating sustained demand for real-time monitoring networks. Local authorities must demonstrate measurable progress on air quality targets — and that requires data from dense sensor networks, not isolated reference stations.

Technology advances

Sensor accuracy and reliability have improved dramatically. Devices like the Sensorbee Air Pro 2 now deliver MCERTS-certified measurements in a compact, solar-powered form factor. This makes dense urban monitoring networks both technically and financially viable — a single unit can be deployed in under five minutes without mains power.

Data-driven policy

Cities are moving from reactive to proactive air quality management. Real-time monitoring data feeds traffic management systems, informs planning decisions, and provides evidence for Low Emission Zone enforcement. The shift from annual reporting to continuous monitoring is creating demand for affordable, always-on sensor networks.

Public awareness

Air quality is increasingly a public health priority across Europe. The WHO estimates that air pollution causes 4.2 million premature deaths globally each year. Citizens expect transparency and real-time access to local air quality data — and cities are responding with expanded monitoring infrastructure.

Sensorbee's position in the market

Sensorbee is profiled in Section 5.5.23 of the report alongside established vendors including Aeroqual, Clarity Movement, Kunak Technologies, AQMesh (Environmental Instruments), Airly, and Oizom. The report profiles 26 companies in the air quality monitoring segment, reflecting a market that remains fragmented with no single dominant player — unlike smart street lighting, where Signify commands a clear lead with 5.8 million installed units.

Being included in a Berg Insight market report is significant. Berg Insight is one of Europe's leading IoT market research firms, with over two decades of coverage across M2M, IoT, and smart city markets. Their inclusion criteria require demonstrated market presence and technology differentiation.

What sets Sensorbee apart in this competitive landscape:

·MCERTS-certified measurements — one of few compact monitoring systems to achieve this UK regulatory standard, ensuring data quality that meets compliance requirements

·All-in-one multi-parameter monitoring — dust (PM1, PM2.5, PM10), noise, vibration, and gas measurement in a single 1.9 kg device, where competitors typically require separate instruments

·Solar-powered as standard — no mains power dependency, enabling deployment at any location including lamp posts, construction perimeters, and temporary installations

·Rapid deployment — operational in under five minutes, purpose-built for both temporary and permanent monitoring networks

·IoT connectivity — NB-IoT and LTE-M for reliable, low-power city-scale networks without WiFi dependency

What this means for the industry

The Berg Insight report validates several points that are important for the air quality monitoring sector and for Sensorbee's stakeholders.

The market opportunity is substantial and accelerating. A 25.2 per cent CAGR makes air quality monitoring one of the fastest-growing segments in the broader smart city ecosystem. The installed base is expected to more than triple from 206,000 to 634,000 units by 2029, with Europe leading adoption.

The market is still fragmented. With 26 profiled vendors and no single dominant player, the competitive landscape favours companies that can differentiate on technology, certifications, and ease of deployment. Market consolidation is expected as the segment matures.

Regulatory tailwinds are strengthening. Stricter EU and UK air quality standards create sustained demand that is not dependent on discretionary budgets. The revised EU Ambient Air Quality Directive and the UK's Environment Act 2021 are structural drivers that will persist through the forecast period and beyond.

IoT infrastructure is maturing. The proliferation of NB-IoT and LTE-M networks reduces deployment barriers and supports dense urban monitoring at scale — moving the market away from expensive, bespoke installations towards standardised, rapidly deployable solutions.

For Sensorbee, this independent market validation comes at a time when the company is expanding its product range, strengthening its certification portfolio, and scaling deployments across Europe. Being recognised alongside established players in a respected market research report underlines our commitment to delivering certified, reliable environmental monitoring technology.

About the report

Smart Cities: Connected Public Spaces – 4th Edition was published by Berg Insight on 11 February 2026. The 270-page report covers five smart city verticals — street lighting, parking, waste management, air quality monitoring, and surveillance — with five-year market forecasts, 123 detailed company profiles, and insights from 50 executive interviews with market-leading companies.

Analysts: William Ankreus and Felix Linderum. The report brochure and table of contents are available for download from Berg Insight's website.

Frequently asked questions

What is the Berg Insight Smart Cities report?

Berg Insight's Smart Cities: Connected Public Spaces – 4th Edition is a 270-page market research report published in February 2026. It analyses five smart city verticals — smart street lighting, smart parking, smart waste management, urban air quality monitoring, and smart city surveillance — with five-year industry forecasts, 123 company profiles, and insights from 50 executive interviews.

How fast is the air quality monitoring market growing?

The global installed base of networked air quality monitoring devices is growing at a CAGR of 25.2 per cent, from 206,000 units in 2024 to a projected 634,000 units by 2029. This is the highest growth rate of any smart city segment tracked in the Berg Insight report, ahead of smart waste management (22.3%), smart street lighting (21.8%), smart parking (17.8%), and smart city surveillance (15.6%).

Why is Sensorbee included in the Berg Insight report?

Sensorbee is profiled in the urban air quality monitoring chapter (Section 5.5.23) as one of 26 vendors. Berg Insight includes companies that demonstrate meaningful market presence, technology differentiation, and relevance to the smart city ecosystem. Sensorbee's MCERTS-certified, multi-parameter, solar-powered monitoring systems meet these criteria.

Which companies are profiled alongside Sensorbee?

The report profiles 26 companies in the air quality monitoring segment, including Aclima, Aeroqual, Airly, Breeze Technologies, Clarity Movement, Ecomesure, Envea, Environmental Instruments (AQMesh), Kunak Technologies, Libelium, Met One Instruments (Acoem), and Oizom, among others. The full list is available in the report brochure from Berg Insight.

Where can I download the Berg Insight report brochure?

The report brochure and table of contents are available for free download from Berg Insight's website. The full report (270 pages, PDF + Excel) can be purchased from their online shop.

David Löwenbrand

Founder & CEO

Ready to Get Started with Environmental Monitoring?

Contact us today to discuss how Sensorbee can help you meet your monitoring requirements.